The biggest challenge of deal flow isn’t finding companies to invest in.

It is finding good companies to invest in.

Just to make the whole process more fun, are no absolutes in angel investing, and it is impossible to define upfront exactly which companies will do well.

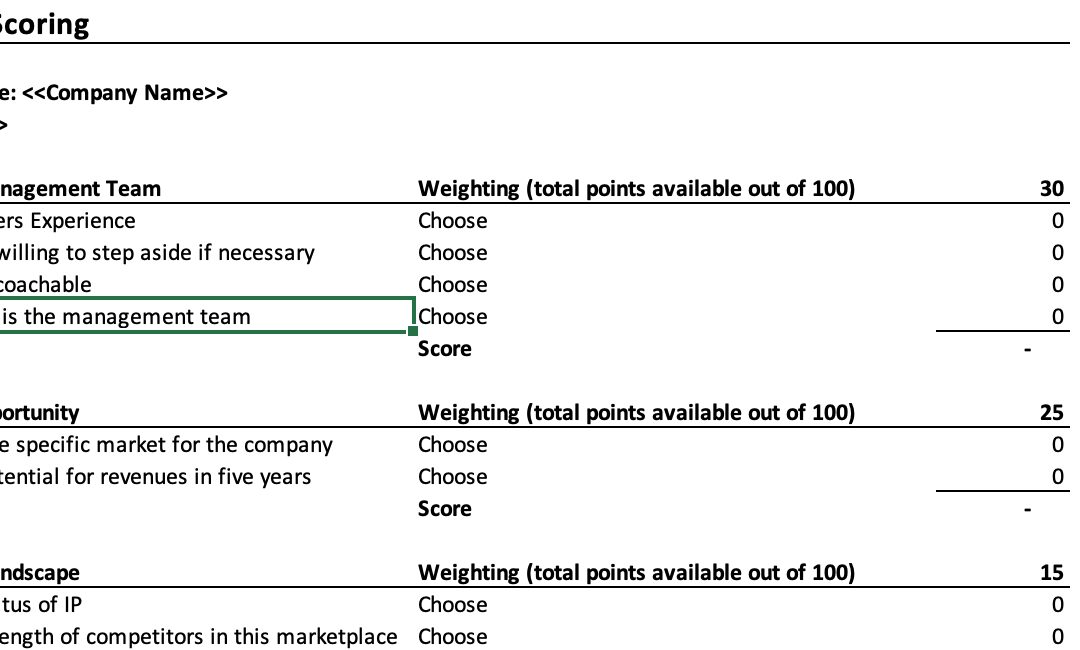

On the other hand, of the hundreds of applications, we get only a handful are worth looking at. One of the ways we evaluate companies is using the criteria in the linked spreadsheet. Download the tool here.

Use this spreadsheet to score companies on a scale from zero to one hundred. A score lower than zero suggests a deal-breaker.

We only use this for early, quick screening not due diligence. We are looking at indicators of performance, and it is based on our experience of what works well in predicting how well companies do with our group.

This is best for excluding companies rather than including them. Inclusion requires significantly more analysis.

Here are the six areas we consider:

Strength of the Management Team

The number one reason early-stage companies fail is market problems. Market problems vary but generally this means:

- The pain doesn’t exist, there is no need for the product – we’ve seen toothpaste dispensers, full-body drum sets designed for exercise and blockchain-enabled ear pods that all claim to be solving a problem none of us could understand.

- The pain may exist but the product does not solve the problem in a compelling enough way to entice buyers. Often the product is too complex or doesn’t work.

- The market pain and product are a fit, but the timing is wrong – think of the Apple Newton. Steve Jobs was on to something, but the market wasn’t ready. He got that right with the iPhone.

Whatever the reason: a bet on a product is dangerous. If the product fails, you’ve lost.

A good team, however, will pivot. Whereas we’ve seen great products go nowhere we’ve seen great teams deliver amazing results with products that seemed, initially, mediocre or uninteresting. We prefer to invest in an “A” team with a “C” product than a “C” team with an “A” product.

At the screening stage, we can’t fully evaluate the team, but the indicators we consider are:

- The founder’s experience.

- The willingness of the founder to step aside and let someone else run the company. (This is an excellent indicator of whether someone is running this for growth or themselves. Unwillingness to step aside is a deal-breaker.)

- Is the founder coachable – “no” is a deal-breaker.

- Completeness of the management (and advisory) team.

Size of the Opportunity

We are not looking for local delis companies that can only serve small, local markets. These “lifestyle businesses” can be great for owner-operators, but they won’t grow enough to provide a return to investors.

We look for a potential for a 30X return on our investment. So the addressable market must be substantial. At least in the hundreds of millions if not in the billions. At the screening stage, we can look at the smaller end, but in due diligence want to see a roadmap to something on the larger side.

We also want to understand the growth potential of the company: will they be able to scale up? Do they have a plan for getting to $30 million in sales over the next five years? Even though this plan is made up, the existence of a plan allows us to see that they are going in the right direction and will enable us to test assumptions.

So the two things we look for here are:

- Size of market

- Potential for revenue within the next five years.

Competitive Landscape

Competition is key: ideally, we want a market where the competition is weak, and the barriers to entry are high. Of course, reality doesn’t ever work that way, so we look for a compromise.

We also consider Intellectual Property here. For some investors, IP is critical, for others, it isn’t. Software patents are usually not very attractive, and most IP can be circumvented, so this isn’t as important an attribute as one might think.

But, some investors only invest in well-protected IP, IP never hurts and in some cases (pharmaceutical for example) it is critical.

Here we look at:

- Status of IP.

- Strength of competitors in the market place.

- Barriers to entry.

Sales Channels

Early companies often don’t even think about sales and marketing. We’d like them to have a plan. We evaluate that by looking at whether they have sales channels in place. Even if they don’t, even if the product is a prototype, we want some idea of how they will get this to the market.

What we consider here is:

- What sales channels are in place?

Business Stage

The more advanced a company, the less the risk. So we ideally want to work with companies that are beyond product development and beginning to sell. Customers and market feedback are ideal, and we think these are strong indicators of whether or not the company produces something the market cares about.

Good, exciting, investments can be earlier in the process, and we have invested in a few; but later is better.

So what we consider here is:

- What stage of business is the company in?

Funding Requirements

Angel investors typically raise less than a million dollars. So we like companies that are in the million-dollar and less range.

Above 1.5 million will be tough. The problem here is ensuring that the startup gets enough funding to achieve their next milestone. If they need too much, can’t raise it and our investment helps them bump along another month, then we have wasted our money.

But the bigger question is: what do they plan to do with the money? We want a clear plan, not just “we are going to keep the business going.” A lack of a clear strategy is a deal-killer. It is generally pretty clear whether or not they have a plan.

So what we look for here are:

- What amount of funding is required.

- Clarity of a plan for funds.

Using the sheet

This spreadsheet is just a tool. It can be useful in screening companies, run through it quickly with each one and you will see that some pop up higher than others. Also, a lot of deal-breakers will show up.

We have created this and adjusted the scoring for the Westchester Angels, and we will change it from time to time. So, do the same for yourself: adjust the scoring and weighting in columns A through F, just unhide them and make the changes you think are appropriate.

And let us know what you think.

Are you interested in learning more about angel investing and how to invest, wisely, as an angel investor?

Check out the boot camp, this rigorous program will get you up to speed and give you the tools you need to make better investment decisions. Angel investing is extremely risky, very challenging and can be a lot of fun. Get the education first – before you make any investments, to give yourself the best chance at success.

Recent Comments